EL CAJON, Calf. —I’m Lizzie Bly. I am not a Dehesa parent. I do not belong to the Dehesa School Parents’ Club. I have never had a student in that district. I am a parent, and I write under a pen name to avoid personal harassment and to ensure my offspring aren’t targeted by proxy because of my investigative reporting. According to multiple parent sources, Superintendent Bradley Johnson appears to believe I’m a Dehesa parent—specifically one of his outspoken critics—and that the Parents’ Club is behind these articles.

If that assumption is being made, it is incorrect—and that potential miscalculation coincided with real-world consequences: the Parents’ Club’s account was frozen the next business day, halting access to funds and stalling planned events.

Friday’s Letters, Monday’s Freeze

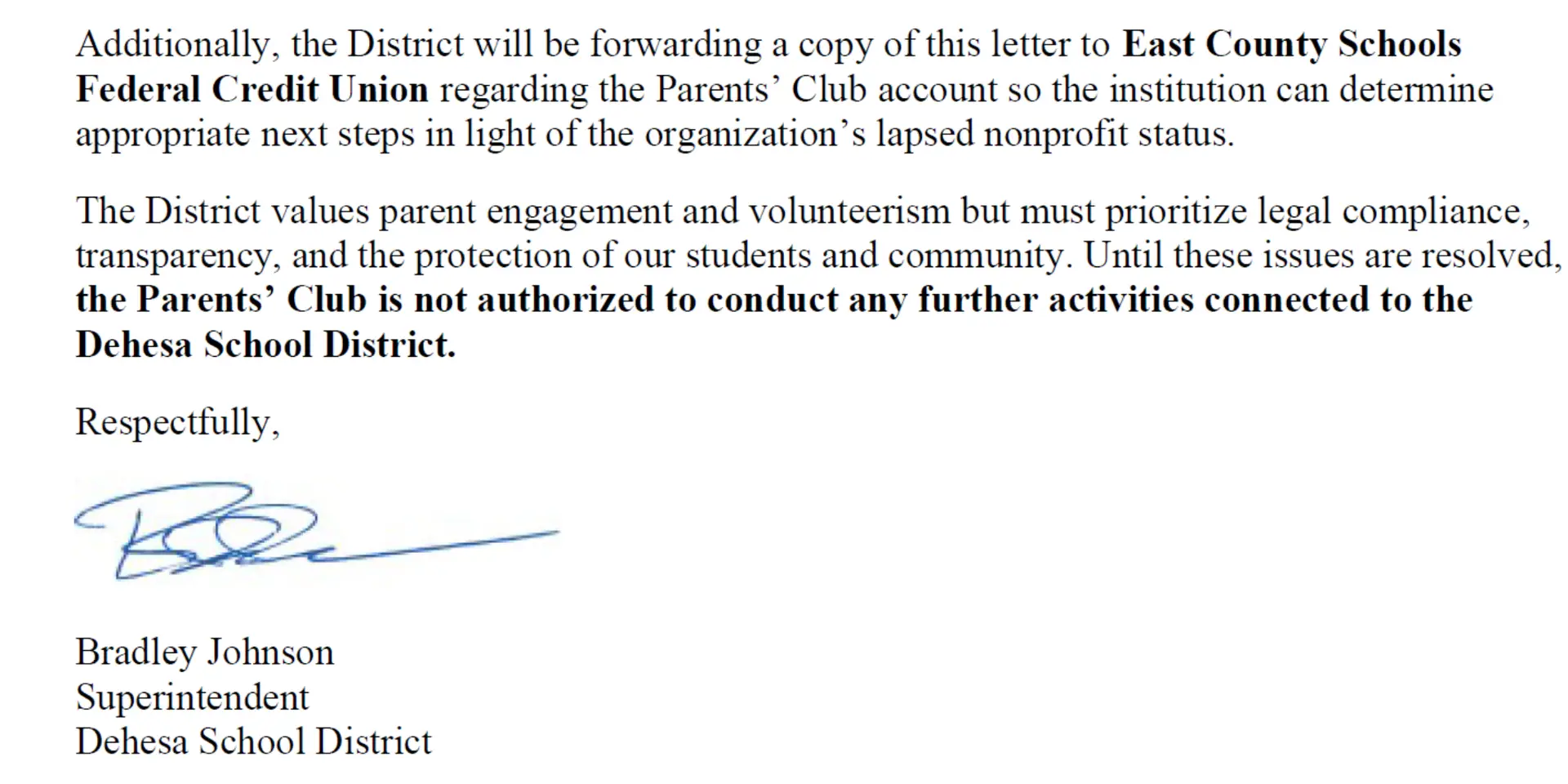

On Friday, August 22, 2025, at around 4:32 p.m. (per the letter timestamp), Johnson issued two communications. The first was a formal “Cease and Desist – Immediate Suspension” to the Dehesa School Parents’ Club, stating the district was cutting the club off from campus activities. In that same letter, he wrote that the district “will be forwarding a copy of this letter to East County Schools Federal Credit Union regarding the Parents’ Club account so the institution can determine appropriate next steps. For context, the credit union closes at 5:00 p.m. on Fridays and reopens Monday morning. The second communication, sent at 4:45 p.m., was an all-community “update” asserting that, during the suspension, the **district—not the parents—**would directly coordinate volunteers and fundraising.

Club officers report that when they went to the credit union the following Monday morning, the account was frozen pending review. Bank staff reportedly said they had “never seen this before”—describing it as a highly unusual situation in their experience. The practical impact was immediate: money raised for kids’ activities was unavailable, and planned events stalled. Access to club documents, assets, and belongings—kept under lock and key on campus—is reported to be limited to a small set of key-holders. Those facts alone would be newsworthy. But there’s a deeper layer the public deserves to know.

Bank Oversight Meets School Politics?

Bradley Johnson sits on the Supervisory Committee of East County Schools Federal Credit Union (ECSFCU)—the very institution he said he would “notify” about the Parents’ Club’s account. ECSFCU’s own site introduces him as Dehesa’s superintendent, a Supervisory Committee member. That overlap matters.

What is a supervisory committee? Under NCUA regulations, it’s the credit union body charged with ensuring accurate financial reporting and safeguarding members’ assets. The duties are narrowly defined: audits, independent account verifications, and investigating bona fide member complaints—governance functions designed to protect the institution and its members, not to referee local political feuds. The federal bylaw framework—Appendix A to 12 C.F.R. Part 701—also speaks clearly: federal credit unions must operate in accordance with their bylaws, and the bylaws prohibit officials from participating in matters that implicate their personal interests, requiring recusal where conflicts exist.

Set alongside those rules, the sequence in Dehesa raises obvious red flags: a superintendent under heavy public criticism tells parents he will “forward” his suspension letter to a credit union on whose oversight committee he serves, and club officers report the account was frozen the next business day. Even if the credit union had grounds to review the account’s paperwork, the messenger matters.

Parents’ Club Fell Behind. That’s Not Evidence of Fraud.

To be fair and accurate: the Dehesa School Parents’ Club did fall out of administrative compliance. Johnson’s letter cites an older IRS revocation and a suspended Secretary of State status, and Registry of Charitable Trusts correspondence on file indicates delinquency notices were mailed to the school address in prior years. These are real lapses—classic small-nonprofit problems when volunteer boards turn over. For tiny groups raising only a few thousand dollars a year, “noncompliant” usually means missed filings, not evidence of fraud. The fix is mechanical: file the retroactive IRS 990-N (e-Postcard) and FTB 199N (e-Postcard), submit the past-due RRF-1 reports to the Attorney General, and update the Statement of Information with the Secretary of State. (Those e-postcards are designed for very small nonprofits—generally those with gross receipts at or under about $50,000 a year.)

In my view, based on the documented sequence above, you pause long enough to let volunteers cure the filings—you don’t drop a public hammer and then route a notice to the bank on your own school’s parent group over fixable paperwork.

The Power Problem

This is where ethics becomes the story. The NCUA’s supervisory framework is built on independence: The committee’s purpose is to ensure that management and the board are following the rules and that member assets are safe. ECSFCU’s own supervisory committee application language underscores that the Supervisory Committee’s responsibilities include: “Oversight for all internal and external examinations to ensure resolution of any exceptions noted; • Carry out duties as a member of the Supervisory Committee in good faith, in a manner you reasonably believe to be in the best interest of the membership;” Nothing in that remit reads as permission for an individual committee member to leverage his credit-union role—or the institution’s processes.

Even if a superintendent is within his authority to pause a parents’ group pending compliance, this wasn’t a defunct club. Club officers say they were actively planning their next event, and nothing in the record suggests an intent to abandon the work, had they been notified on August 6, the Parents’ Club asserts they would have taken steps to remedy the situation right away. Against that backdrop, the sequence reads less like neutral housekeeping and more like public signaling with punitive effect—suspension first, then a bank notice.

And the speed matters. Per the documents, the cease-and-desist went out late Friday; by Monday morning, officers report the account was already frozen. That looks like a rapid response to a single notice—from a superintendent who also sits on the credit union’s oversight body. Reasonable readers will wonder: would the same timeline have unfolded if the email had come from an ordinary member on a Friday at 4:32 p.m.? Was there any independent vetting beyond the one notice, or did the sender’s stature do the work? On the record before me, it appears the administrative process became the vehicle—and the bank, the unwitting cog, only following policy—for a result that likely would not have arisen organically.

The federal bylaws framework matters, too. Federal credit unions must follow their bylaws, and those bylaws generally prohibit officials from participating in matters that touch their pecuniary or personal interests—that is, where the official has a personal stake or reputational entanglement. In my view, a superintendent taking steps that affect a parents’ group whose members have publicly called for his resignation reasonably implicates a personal interest. Even if Johnson took no part in ECSFCU’s internal handling after hitting “send,” the appearance of influence created by his dual role is substantial.

“But rules are rules.” Selective zeal is still zeal.

Johnson appears to have framed this as simple rule-enforcement: the club was out of compliance, therefore suspension, I wouldn’t bat an eye at that move alone. However, the bank notice is not typically seen as standard practice by an average superintendent; otherwise bank staff would have been able to readily address it, without the need for legal. Given that a vice president—a role that typically reflects long service—states they had never experienced this, it suggests this is an extraordinary move that isn’t standard practice. But standards apply to superintendents, too. California law bars public officials from using public resources for personal purposes. That includes official time and email systems. If the bank notice was hatched and transmitted using district resources to advance what looks like a personal vendetta against critics, that’s not bold leadership; that raises legal and ethical concerns under California’s rule against using public resources for non-official purposes.

And context matters. Dehesa is a tiny school—roughly 60 RESIDENT students (charter enrollment increases topline figures and can blur lines between in-district resident students and charter enrollment). According to the Parents’ Club officers, balances have historically been in the low thousands; no one is buying yachts with bake-sale money. Low thousands can still be a lot of money, but in this case the amounts raised yearly by the Parents’ Club are typically less than ~$4,000 annually. By choosing what appears to be public shaming + bank freeze over quiet coaching + cure, Johnson appears to have sent a message that compliance is a weapon, not a standard. Parents heard it loud and clear.

Organic Decision—or Engineered Outcome?

Yes—the Parents’ Club acknowledges its current delinquency and understands a financial institution must follow its own guidelines. They don’t fault the bank for having compliance rules, and they’re already working to restore status. But the question is whether this freeze would ever have materialized organically, absent a nudge from a superintendent with skin in the game. One can read the answer in the bank’s own reaction: according to contemporaneous notes from club officers, bank management called the situation “highly unusual,” said they had never seen it, and noted they had to reach out to legal for next steps; during the visit, the teller couldn’t even pull up the account without management-level access. That is not the texture of what feels like a routine compliance trigger; to a reasonable reader, it looks like what an institution appears to do when reacting to an external shove, not executing a well-worn policy pathway.

And that’s the real harm. The Parents’ Club accepts the legal housekeeping they need to do. What they can’t accept—and what the community shouldn’t accept—is an outcome that appears not to have arisen organically, not plainly merited by standard policy alone. Absent Bradley Johnson’s intervention, this likely would not have happened—at least not like this and not on this timetable. The bank vice president’s reported words—“never seen this”—speak louder than any op-ed. On the surface, this does not read like a routine, organic compliance action; the timing suggests his dual role may have influenced how this unfolded.

Did The Bank Even Know? And What Do They Say Now?

ECSFCU has a long, stellar reputation as the educators’ bank—for teachers, bus drivers, cafeteria workers, and the people who support them. Which is why this feels out of their norm.

There is a simpler, human version of all this: Would the credit union be proud to tell every member—teachers, bus drivers, cafeteria workers—that it froze a school parents’ account over fixable paperwork soon after a controversial superintendent sent a letter? Would the board say, on the record, that this is the kind of judgment they expect from their own committee members—that this is how you treat the people who hold bake sales so a classroom can afford art supplies? If the honest answer is no, then it appears the institution didn’t co-sign the lead-up; it simply fulfilled a legal or policy duty to freeze once notified of the club’s status—an outcome that likely would not have arisen on this timetable absent Mr. Johnson’s notice.

The Retaliation Lens

You don’t need a constitutional law course to see the concern: based on the documented sequence, a public official facing criticism took steps that coincided with a parents’ group losing campus standing and club officers reporting that its funds were frozen; in his letter, he stated he would “notify” the bank where he also serves on an oversight committee. In First Amendment terms, that creates retaliation optics—adverse action closely following protected speech. Even if lawyers might debate the doctrine, the community standard is simpler: this isn’t how you treat your own parents.

Taking a Page from Johnson’s Rulebook

If this is being framed as “rules are rules,” then let’s apply them evenly. In my view, and based on the facts set out above, when a public official appears to wield overlapping positions to influence a private institution’s decision about a tiny parent nonprofit, that’s not just bad optics—that’s a reportable concern. It is appropriate to raise such concerns with credit-union leadership, the NCUA, and the District Attorney’s Public Integrity Unit. Parents who feel affected can, in good faith, petition those bodies and share truthful information—petitioning the government on a matter of public concern is protected speech (and in California, activity of this kind is protected by the anti-SLAPP statute).

Meanwhile, The Kids

The hardest part to swallow is the impact where it always lands—in kids’ experiences. The core of what parent volunteers do, what they are on that campus raising money for in the first place, the kids. When associations that strive to support and for the betterment of the school is abruptly removed from a campus with no remedy of relief, activities like field trips don’t happen; teacher mini-grants don’t go out; the fall carnival looks shaky. Parents work long hours and still show up to stuff envelopes and grill hot dogs. They’re volunteers, not compliance officers. They are neighbors trying to make a small school feel big with love. In my opinion, a superintendent’s first instinct should be to help them fix what’s broken—not to trigger a bank hold and call it accountability.

What Accountability Should Have Looked Like:

For Dehesa School District: acknowledge the paperwork facts and set a 30-day cure window with a clear checklist, then step back and let parents be parents.

For ECSFCU: treat the freeze as a compliance event. To ensure this does not become problematic for ECSFCU, review what came in, how it came in, and whether any recusal was warranted and, if so, documented for a Supervisory Committee member with a personal/professional stake. The NCUA’s standards exist for a reason. Parents have no suggestion of impropriety on part of the credit union, in fact they recognize the policy in place, and the bank’s position in the matter, their hands are tied, and must uphold compliancy, in spite of the spirit of delivery.

For the board that continues to approve his employment: in my view, this is why appointing leaders who lack required credentials and serve on waivers usually breeds crisis, not competence. You are elected officials—accountable to families, not to any one administrator. Convene a neutral, independent investigation, require recusals where appropriate, preserve records, and report your findings publicly. Club members and supporters are calling on Board President Cindy White: do not ignore this. Lead a fair process, follow the facts, and act—or your constituents will hold you accountable.

For Superintendent Johnson: stop mistaking criticism for disloyalty. Your job isn’t to win; it’s to serve. As a taxpayer, sit down, step back from any conflicts, and do the work—or make room for someone who will. Time to serve is now, BJ.

Evidence Attached: